New or used, work or play. Let the HarborLight Credit Union lending experts find the funds you need for the ride you want.

Key Features

-

Competitive Rates

Competitive Rates

-

Free Pre-Approval

Free Pre-Approval

-

Rate Reduction Available

Rate Reduction Available

- Competitive rates

- Convenient terms customized to fit your budget

- Pre-approval available for extra bargaining power at the dealership

- Refinance your current loan to potentially lower your rate

- Local decision-making and processing

- Attentive, friendly service from start to finish

GAP Waiver Protection

GAP Waiver provides supplemental protection to a borrower’s primary insurance and is designed to help borrowers avoid financial loss in the event of total loss or unrecovered theft. The difference between the loan net payoff amount and the actual cash value (ACV) paid by the primary insurance settlement produces a deficiency balance or “gap.” This remaining loan balance is covered (or waived) with GAP protection.

Additional Benefits

- Saves money by reimbursing the insurance deductible (up to $500) when a deficiency balance remains after a total loss

- Eliminates risk of negative equity

- Gives instant equity with $1000 for a replacement vehicle when financed by same lender

- Provides a positive, quick and fair claims experience

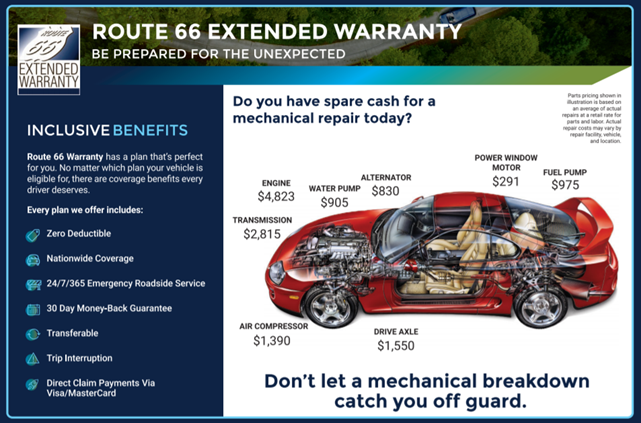

Mechanical Repair Coverage

Even the most reliable vehicle can develop a mechanical problem. That is why so many people have come to depend upon Route 66 Warranty.

Route 66 Warranty is the most comprehensive vehicle service contract with coverage available for all automobiles so that you will be able to enjoy your new purchase and have "Peace of Mind."

No matter where you travel in the United States, you are protected against major mechanical expenses, and there is no deductible on covered parts and labor.

Key Benefits of Route 66 Warranty*:

- Route 66 Warranty has over 33 years experience

- All plans have a $0 deductible

- 30-day money-back guarantee

- Nationwide coverage

- Route 66 works with any certified mechanic of your choice

- 24/7/365 Emergency Roadside Service with EVERY plan

- Plans are transferable if you sell your car

- All plans come with rental and trip interruption benefits

- All vehicle service contracts are fully insured

*Program details may vary by state. Ask a Member Services Representative for details or receive a quote by calling (877) 894-5557.

Debt Protection

Help protect your family against the unexpected.

Life can be wonderful. But it can also get complicated when unexpected things happen. Protecting your loan balance or loan payments against death, disability or involuntary unemployment could help protect your finances.

Call HarborLight Credit Union at (877) 894-5557 and ask about protecting your loan today.

Your purchase of Debt Protection is optional and will not affect your application for credit or the terms of any credit agreement required to obtain a loan. Certain eligibility requirements, conditions, and exclusions may apply. Please contact your loan representative, or refer to the Member Agreement for a full explanation of the terms of Debt Protection. You may cancel the protection at any time. If you cancel protection within 30 days you will receive a full refund of any fee paid.

DP-2045000.1-0318-0420 © CUNA Mutual Group 2018, All Rights Reserved.